Blockchain gives us the technology to move information securely, and gives us almost complete confidence in the authenticity of any piece of information you want to protect. Blockchain is currently used by only 1% of the world's population. Let's take a look at why this technology could take the world by storm.

Brief Definitions of Blockchain

Blockchain is a technology for storing data that is stored in a chain of sequentially linked blocks on computers. Each block contains a unique code called a hash. It also contains the hash of the previous block in the chain. Once an entry is added to a chain, it cannot be changed. Hence the name block (block) and chain (chain).

Blockchain is the underlying technology that powers many cryptocurrencies such as Bitcoin and Ethereum, but its unique way of securely recording and transmitting information has wider applications outside of cryptocurrency.

Blockchain is a type of distributed ledger. Distributed ledger technology (DLT) allows accounting to be maintained across multiple computers, known as “nodes” or “nodes.” Any blockchain user can be a node, but it requires a lot of computer power to operate. Blockchains can be open (public) or closed.

Essence:

- Blockchain is a special type of database.

- It differs from a regular database in the way it stores information; Blockchain stores data in blocks, which are then linked together.

- As new data arrives, it is entered into a new block. Once a block is filled with data, it is linked to the previous block, resulting in the data being chained together in chronological order.

- Blockchain can store various types of information, but by far the most common use remains as a ledger for cryptocurrency transactions.

- In the case of Bitcoin, the blockchain is used in a decentralized manner so that no one person or group of individuals has control—or rather, all users collectively retain control.

- Decentralized blockchains are immutable, meaning that the data entered cannot be changed. For Bitcoin, this means that transactions are constantly recorded and can be viewed by anyone.

Prospects

Chia mining on hard drives has attracted widespread interest, but at the same time there have also been accusations towards hardware manufacturers - the latter are suspected of fueling interest in XCH mining, which may fade after manufacturers carry out plans to sell off storage drives.

The IOU XCH rate remains unstable - a sharp rise with the launch of trading on Hotbit was followed by a halving of the price, despite the support of the more famous Gate.io.

Among the factors that will help maintain the positive momentum is the presence of its own language, Chialisp, with potential applications in the decentralized finance, or DeFi, sector.

How is blockchain used?

Blockchain technology is used for many different purposes, from providing financial services to administering voting systems. Let's look at real examples of use.

Cryptocurrency

Most often, blockchain is used today as the basis of cryptocurrencies such as Bitcoin or Ethereum. When people buy, trade on exchanges, or spend cryptocurrency, the transactions are recorded on the blockchain. The more people use cryptocurrency, the more widespread blockchain may become.

“Because cryptocurrencies are volatile, they are not yet widely used for purchasing goods and services. But that's changing as PayPal, Square and other money services businesses make digital asset services widely available to providers and retail customers."

says Patrick Dougherty, senior partner at Foley & Lardner and head of the firm's blockchain task force.

Banking

In addition to cryptocurrency, blockchain is used to process transactions in fiat currencies such as dollars and euros. This can be faster than sending money through a bank or other financial institution because transactions can be verified faster and processed outside of normal business hours.

Transfer of assets

Blockchain can also be used to record and transfer ownership of various assets. This is currently very popular with digital assets such as NFTs, digital art ownership representation, and videos.

However, blockchain can also be used to process ownership of real assets, such as real estate. Both parties will first use the blockchain to verify that one of them owns the property and the other has the money to purchase; they could then complete the transaction and record the sale on the blockchain.

Using this process, they could transfer ownership without manually submitting documents to update the local registry. The data will be instantly updated on the blockchain.

Smart contracts

Another innovation in blockchain is self-executing contracts, commonly referred to as “smart contracts.” These digital contracts come into force automatically once the conditions are met. For example, payment for goods can be made instantly as soon as the buyer and seller comply with all specified parameters of the transaction.

“We see great potential in the field of smart contracts - using blockchain technology and software instructions to automate legal contracts,”

said C. Neil Gray, fintech partner at Duane Morris LLP.

“A properly drafted smart legal contract on a distributed ledger can minimize, or preferably eliminate, the need for data verification by external third parties.”

Supply chain monitoring

Supply chains involve enormous amounts of information, especially when goods move from one part of the world to another. With traditional data storage methods, it can be difficult to trace the source of problems, such as from a supplier of substandard goods.

Storing this information on the blockchain will make returns and supply chain monitoring easier, such as with the IBM Food Trust, which uses blockchain technology to track food from harvest to consumption.

Vote

Experts are looking for ways to use blockchain to prevent voting fraud. In theory, blockchain voting would allow people to cast votes that cannot be tampered with, and would also eliminate the need for people to manually collect and verify paper ballots.

Benefits of Blockchain

Higher transaction accuracy

Since a blockchain transaction must be verified by multiple nodes, this can reduce the number of errors. If one node has an error in the database, other nodes will see it and not make the error.

In contrast, in a traditional database, if someone makes a mistake, they may be more likely to repeat it. In addition, each asset is individually identified and tracked on the blockchain ledger, so there is no chance of so-called double spending (for example, if a person overdrafts their bank account, thereby spending money twice).

No need for intermediaries

Using blockchain, two parties to a transaction can confirm and complete something without having to work through a third party. This saves time, as well as the cost of paying for the services of an intermediary such as a bank.

Extra Security

In theory, a decentralized network like blockchain makes it virtually impossible for fraudulent transactions to occur. To introduce fake transactions, they would need to hack every node and change every “ledger.”

Many cryptocurrency blockchain systems use algorithmic or “proof of work” transaction verification methods that make it difficult to add fraudulent transactions.

More efficient translations

Because blockchains operate 24/7, people can transfer funds and assets more efficiently, especially internationally. They don't have to wait days for a bank or government agency to manually approve everything.

Disadvantages of Blockchain

Limit of transactions per second

Be sure to read: The main problems of Bitcoin. How to solve them?

Given that the blockchain depends on a larger network to approve transactions, there is a limit to how quickly it can move.

For example, Ethereum can only process 20 transactions per second versus Visa's 1,700 transactions per second. In addition, an increase in the number of transactions may cause problems with network speed. Until this improves, scalability will be an issue.

High energy costs

Running all the nodes to validate transactions requires significantly more power than a single database or spreadsheet. This not only makes blockchain-based transactions more expensive, but also creates a large carbon burden on the environment.

Because of this, some industry leaders are starting to move away from certain blockchain technologies such as Bitcoin: for example, Elon Musk recently said that Tesla would stop accepting Bitcoin in part because he is concerned about the damage to the environment.

Risk of loss of assets

Some digital assets are protected using a private key. You need to guard this key carefully.

“If the owner of a digital asset loses the private cryptographic key that gives him access to his asset, there is currently no way to recover it - the asset is lost forever,”

says Gray. Because the system is decentralized, you cannot call a central authority, such as a bank, to request access to be restored.

Possibility of illegal activities

Blockchain decentralization adds more privacy and anonymity (see list of anonymous cryptocurrencies), which, unfortunately, makes it attractive to criminals. It is more difficult to track illegal transactions on the blockchain than through bank transactions linked to a name.

Key Features

- Limit - the supply is limited to 21,000,000 XCH, of which 19,000,000 belongs to the developers.

- Security - based on the unique PoST protocol. The system is resistant to ASIC mining, which protects against the concentration of coins in the hands of one mining pool.

- Open Source - Chia Blockchain code is available on GitHub.

- Multiplatform—Windows, macOS, and Ubuntu Linux users can interact with Chia. For the latter, the work will be especially comfortable, because Python is the native language of Ubuntu.

How does Blockchain work?

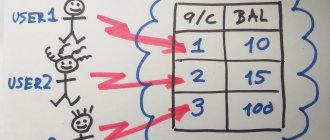

As mentioned above, nodes or “nodes” verify, approve, and store data in a ledger. This differs from traditional record keeping methods, in which data is stored in a centralized location, such as a computer server.

Blockchain organizes information added to the ledger into blocks or groups of data. Each block can only contain a certain amount of information, so new blocks are constantly added to the ledger, forming a chain.

Each block has its own unique identifier - a cryptographic “hash”. The hash not only protects the information in a block from anyone who does not have the necessary code, but also protects the block's place in the chain by identifying the block that came before it.

A cryptographic hash is “a set of numbers and letters that can be up to 64 digits in length. This is a unique code that allows the puzzle pieces to fit together.

Once information is added to the block chain and encrypted with a hash, it becomes permanent and immutable.

Each node has its own record of the complete timeline of data on the blockchain, starting from the beginning. If someone tampered with or hacked one computer and manipulated the data for their own gain, it would not change the information stored on other nodes. The modified entry is easy to identify and correct since it does not correspond to the majority.

Understanding the Consensus Mechanism

The peer-to-peer network mechanism was used back in 1999 by Napster (a file-sharing peer-to-peer network).

Blockchain also existed before Bitcoin.

The genius Satoshi Nakamoto , the mysterious and anonymous founder of Bitcoin, combined blockchain with a cryptography-based consensus mechanism. The consensus mechanism is where the real magic happens: it allows nodes in a peer-to-peer network to work together without knowing or trusting each other.

“The purpose of a consensus algorithm is to provide a secure update of state according to some specific state change rules, where the right to perform a state change is distributed among (...) users who are granted the right to collectively perform the change through the algorithm” - Vitalik Buterin

Now, if you haven't quite figured it out, a consensus mechanism is simply a set of rules that are agreed upon by nodes on a network by running the network's software . These rules ensure that the network operates as intended and remains in sync.

The Consensus Protocol sets the rules:

- How should blocks be added to the blockchain?

- when blocks are considered valid, and

- how conflicts are resolved.

Example of work

Here is an example of how blockchain is used to verify and record Bitcoin transactions.

A consumer buys Bitcoin.

Transaction data (TXID) is sent through Bitcoin's decentralized network of nodes.

Nodes confirm the transaction.

Once approved, the transaction is grouped with other transactions to form a block, which is added to the ever-growing chain of transactions.

The completed block is encrypted and the transaction record is permanent; it cannot be deleted or changed on the blockchain.

In technical terms, blockchain works as follows:

Receipt of information (info) into the blockchain. The information can be: a financial transaction (for example, confirmation of a transaction), user identification (for example, logging into a social network), etc. It depends on the idea of creating a blockchain. 1 blockchain = 1 type of information.

Verification and confirmation of the truth of information. When new information enters the blockchain, it must be checked for truth and confirmed by all users of the blockchain (the equipment connected to the blockchain acts as users, so all operations are performed instantly). In mining, verification and confirmation of information, which entails the creation of a block, can be carried out in two fundamentally different ways: PoS and PoW. Read more here.

Creating a block. Once all users of the blockchain have confirmed the truth of the information, a block is created that includes several pieces of information (for example, several transactions). Each block carries not only the received information, but a timestamp and a link to the previous block, that is, the contents of each block can be checked. This ensures that each block is persistent, meaning the block cannot be changed.

Inclusion of a new block in the chain. A new block is sequentially added to the chain of similar blocks. The block chain contains information about all transactions ever performed in the database. The entire chain with the same set of information is stored by each blockchain participant on many computers around the world.

Image enlarges by clicking

The peculiarity of blockchain technology is that information is stored not on one server, but on different ones that are not interconnected - such a system is called decentralized, that is, without a common center.

At its core, blockchain technology is similar to the Internet: the user posts information, it is verified, and all users have access to the verified information. It is impossible to rewrite the information in a block, since changing any block will lead to changes in the entire chain, and since the chain is stored on many computers, the information in it will be different, and other participants in the chain will simply ignore it (for them it will be incorrect).

In other words, the authenticity of every block is verified against every block chain on every computer. This means that the blockchain cannot be hacked.

All cryptocurrencies operate on blockchain technology, financial transactions are carried out with real money in banks, and much more. This technology, although it has a number of shortcomings, has a great future ahead of it, as special centers are being created for its development and improvement. Blockchain is firmly entrenched in global communities.

Where to store

You can store XCH on a wallet that is part of the official software for miners - Chia Blockchain.

Useful link : https://www.chia.net/ru/ (official website of the project).

This is where the wallet is for now. Source:.chia.net

XCH wallets are not supported by third party developers due to the lack of coins available.

Blockchain Databases

Blockchain sounds complicated, and it certainly can be, but its core concept is actually quite simple. Blockchain is a type of database. To understand blockchain, you must first understand what a database actually is.

A database is a collection of information that is stored electronically in a computer system. Information or data in databases is usually structured in a tabular format to make it easier to search and filter specific information.

What is the difference between using a spreadsheet to store information rather than a database?

Spreadsheets are designed for one person or a small group of people to store and access limited amounts of information. In contrast, a database is designed to house significantly larger volumes of information that can be accessed, filtered, and processed quickly and easily by any number of users simultaneously.

Large databases achieve this by storing data on servers that are made of powerful computers. These servers can sometimes be built using hundreds or thousands of computers to have the processing power and storage capacity needed to allow many users to access the database simultaneously. Although a spreadsheet or database can be accessed by any number of people, it is often owned by the business and managed by a designated person who has full control over how it operates and what data is stored in it.

Blockchain storage structure

One of the key differences between a typical database and a blockchain is the way the data is structured. Blockchain collects information together into groups, also known as blocks, which contain sets of information.

Blocks have a specific storage capacity and, when full, are linked to a previously filled block, forming a chain of data known as a “Blockchain.” All new information that follows this newly added block is compiled into a newly formed block, which will then also be added to the chain once complete.

A database structures its data into tables, while a blockchain, as its name suggests, structures its data into chunks (blocks) that are connected together. It turns out that all blockchains are databases, but not all databases are blockchains.

This system also inherently creates an irreversible data timeline when implemented in a decentralized manner. Each block in the chain receives an exact timestamp when it is added to the chain.